This article is also available in Spanish.

In a note published on Tuesday, Jurrien Timmer, director of Global Macro at Fidelity Investments, discusses how the changing economic landscape can affect markets, central bank policy and the trajectory of both bitcoins and gold. When the S&P 500 reaches modern ups and the so -called “Trump Trade” reversal course, Timmer offers a detailed insight into fiscal policy, inflation and role of risk assets in the “limited” market environment.

Trump effect

Wood Observes that the first six weeks of 2025 brought unexpected market movements and an extremely high “noise ratio to signal”. The dominant expectations of the market coming throughout the year – marking “higher yields, a stronger dollar and exceeding American actions” – he suddenly reversed. He notes: “It seems that in 2025, that the trade in consensus with higher yields, a stronger dollar and the elevation of American shares transformed into the opposite.”

Timmer emphasizes that Bitcoin, freshly from the rally at the end of the year, remains up to date with three -month return rankings, and then carefully with gold, Chinese actions, goods and European markets. At the bottom of the table, American dollar and treasures come out.

Despite the S&P 500 records, Timmer calls this “digestion period” after optimism after the election. He explains that the market under the header is much less decisive. According to Timmer, the parallel index remains suspended, and only 55% of shares trade above their 50-day average movable.

“The sentiment is stubborn, credit spots are narrow, the capital risk bonus (ERP) is in the 10th decil, and VIX is 15 years. The market seems to be priced for success. ” Timmer emphasizes that although the enhance in earnings was solid at 11% in 2024, the searches seem delicate and there are open questions about what could happen if long -term rates enhance in the direction of 5% or more.

One of the most significant elements of Timmer’s analysis in the federal reserve policy. It points to a recent CPI report, with an annual number of basic inflation of 3.5%, as an indicator of almost a consensus that the Fed will remain at the break. “It is already unanimous that the Fed is suspended for some time. In my opinion, exactly so. If the neutral is 4%, I believe that the Fed should be Smidge above this level, taking into account the potential probability that “3 is modern 2.” “

He warns against the possibility of “premature turnover”, recalling policy errors from 1966–1968, when the rate reductions occurred too early, ultimately allowing inflation for usefulness.

From the Fed apparently resulting from the side, Timmer believes that the next market factor for interest rates will come from the long end of the curve. In particular, he sees the tension between the two scenarios: one with endless deficits and growing term contributions-own capital contributions-and another emphasizing fiscal discipline, which would probably limit itself with long-term yields of bonds.

Timmer also notes that weekless unemployment claims can focus on bond markets, taking into account how government expenditure under the modern administration can affect employment data.

Timmer points to a potential stubborn pattern-on the bottom of the head and shoulders-in the point index of the Bloomberg goods. Although it ceases to name this final change, he notes that the goods remain in a wider secular height and may observe the renovated interest of investors if the inflationary pressure remain increased or the fiscal conditions remain loose.

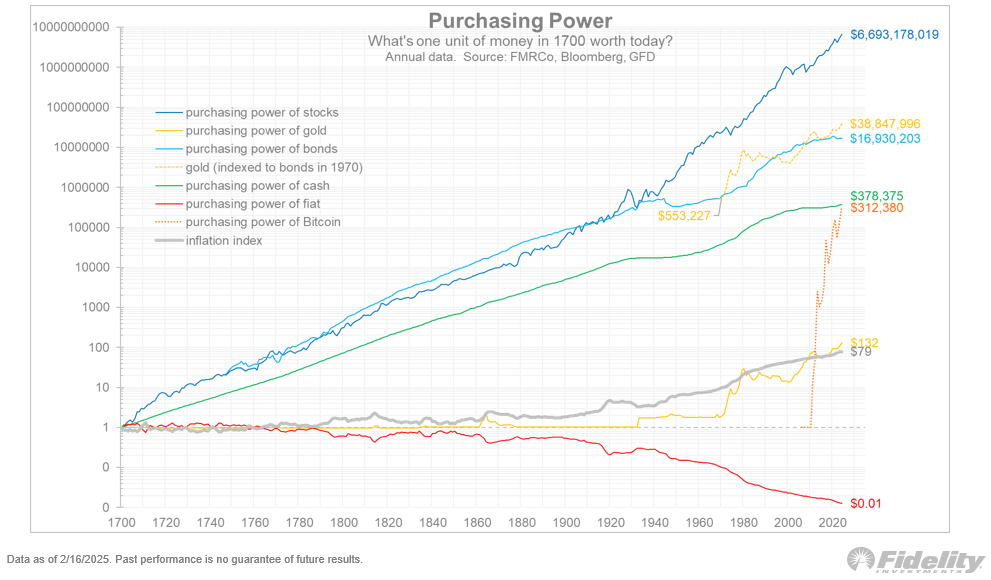

Note, as he notes, he was a “great winner” in recent years, exceeding the expectations of many skeptics: “Since 2020, Gold has brought almost the same turn as the S&P 500, at the same time with lower variability. In my opinion, gold remains an indispensable element of the diverse portfolio in the regime, in which the bonds may remain impaired. “

Timmer sees that gold is testing a critical level of USD 3000 among the global enhance in money supply and a decrease in real crops. Historically, gold showed a mighty negative correlation with realistic profitability, although Timmer believes that the strength of slow metal can also reflect fiscal fiscal dynamics than cash dynamics – especially geopolitical demand for central banks in China and Russia.

Bitcoin vs. Gold

According to Timmer, better results of both gold and Bitcoin “caused many conversations about cash inflation.” However, it distinguishes “the amount of money” (money supply) and the “price of money” (price inflation).

“The purpose of this exercise is to demonstrate that the increase in traditional assets prices over time can not simply be explained by the cash debt (which is the favorite entertainment of some bitcoiners)” – he writes.

Timmer charts suggest that while the nominal M2 and nominal GDP have been blocking for over a century, consumer price inflation (CPI) remained a bit delayed by the enhance in money supply. He warns that adaptation of assets only to M2 may be required.

Despite this, his analysis states that both Bitcoin and Gold have mighty correlations with M2, although in various ways: “It is interesting that there is a linear correlation between m2 and gold, but the power curve between M2 and Bitcoin. Different players in the same team. “

Timmer has emphasized Gold’s long-term results since 1970, noting that he effectively kept the tempa-and he even exceeded the value created by many bond portfolios. He considers the role of Gold as “security against bonds”, especially if sovereign debt markets remain pressure by fiscal deficits and higher long -term rates.

Timmer’s note emphasizes that good Bitcoin results cannot be seen in isolation from gold or a wider macroeconomic environment. With the performance of stream and decision -makers struggling with deficits, investors may be forced to re -assess the customary 60/40 portfolio model.

He emphasizes that although earlier extensions of the cash supply often caused inflation, the relationship is not always one on one. Bitcoin’s meteoric growth may, according to Timmer, reflect the perception of the market that fiscal fears – not only monetary policy – are raising the prices of assets. “As you can see from a dotted orange line and green line, Bitcoin added the same value as over 300 years of age,” he concluded.

During the BTC press it traded for USD 95,700.

A highlighted image from YouTube, chart from tradingview.com